Diamond miners are postponing sales and reviewing their production plans amid the weak market environment.

“We have taken the proactive decision to defer the upcoming August-September tender from our South African operations, to support steps taken by major producers to restrict supply in this weaker demand period,” Petra Diamonds said in an August 6 statement.

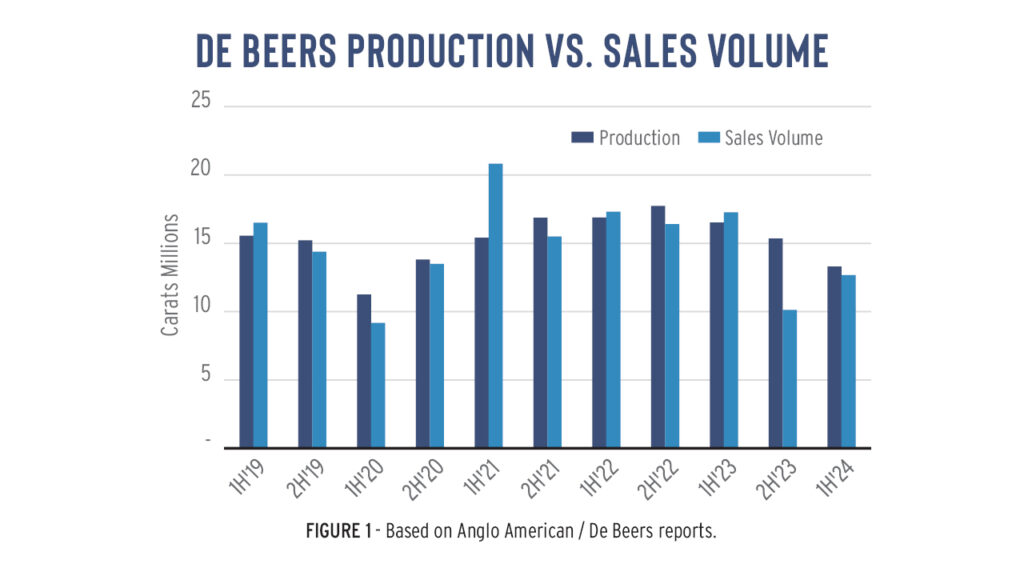

Yet Petra wasn’t the first mining company to withhold goods in the current sales cycle. De Beers allowed sightholders to refuse more of their allocations than usual and raised the threshold for buybacks at its July sight. It’s also combined its August and October sights into one sale, which will take place in September — just before the Diwali break.

In other words, De Beers is selling less than planned. This, after rough sales dropped 22% year on year to $1.95 billion in the first half of 2024, with volume down 26% to 12.7 million carats, the company reported in July. Its rough price index declined 20%.

De Beers continues to build inventory, as production exceeded sales by around 624,000 carats in the first six months of the year. Its stockpiles were already bloated at the beginning of the year, valued at $1.7 billion at the end of 2023, CEO Al Cook revealed.

In addition to allowing sightholders to buy less, De Beers reduced its production program for the year. It now expects to recover 23 million to 26 million carats in 2024, rather than the 26 million to 29 million carats it previously planned. It recovered 31.8 million carats in 2023.

Historic lows

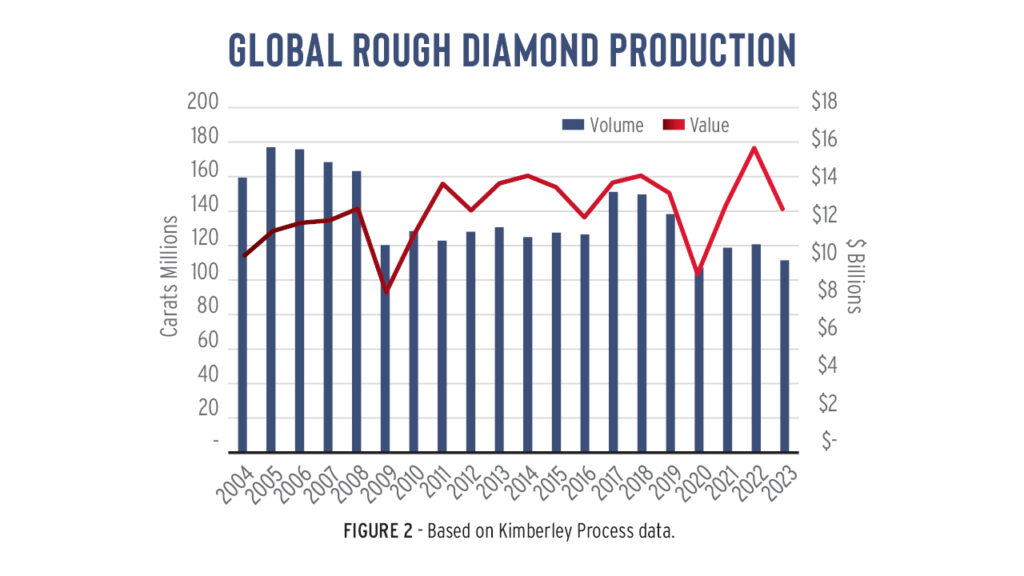

With De Beers taking the lead, global diamond production is therefore on track to drop further in 2024 after hitting historic lows last year.

Total output fell 8% to 111.5 million carats in 2023, according to data the Kimberley Process (KP) published in early July. That’s the lowest level on record since the organization began publishing data some 20 years ago — that is, apart from 2020 when mines had to close during Covid-19. By value, production dropped 20% to $12.73 billion as the average price declined 14% to $114 per carat.

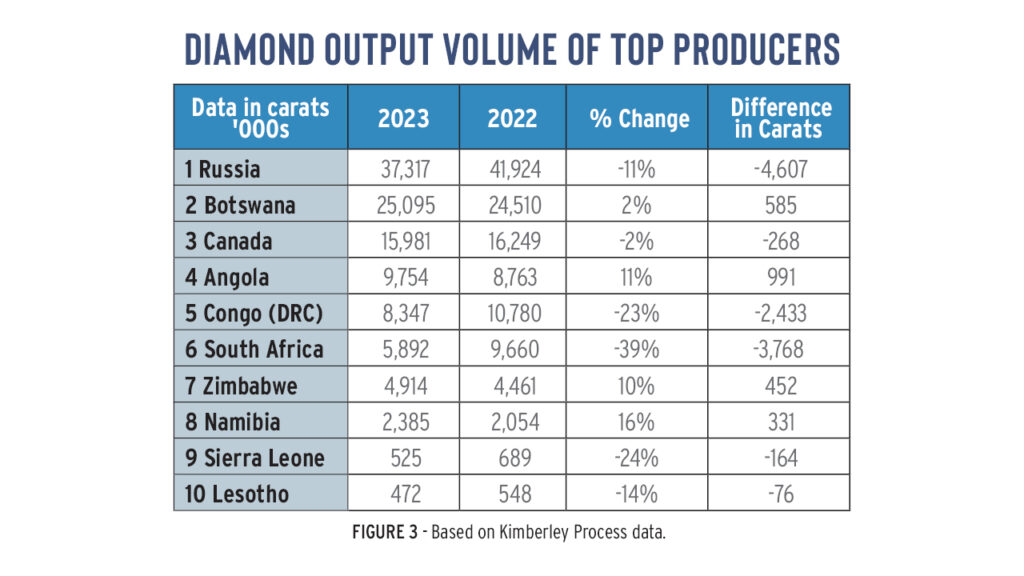

The biggest contributors to the decline were Russia, South Africa and the Democratic Republic of the Congo (DRC). Russia’s diamond output fell 11%, or by 4.6 million carats, although it ranked as the top producer by volume and value. South Africa’s production was 3.8 million carats below 2022 levels, and the DRC — which recovers low-value rough — fell by 2.4 million carats.

Details about Russia’s diamond-mining program have been restricted since the war in Ukraine began. The country exported 87% of its production, despite sanctions imposed on its diamonds, the KP data revealed. That’s just below the annual average of 92% that it exported over the past 20 years.

Operational factors impacted South Africa, given the declines that were anticipated at the De Beers-owned Venetia deposit during its transition to underground mining.

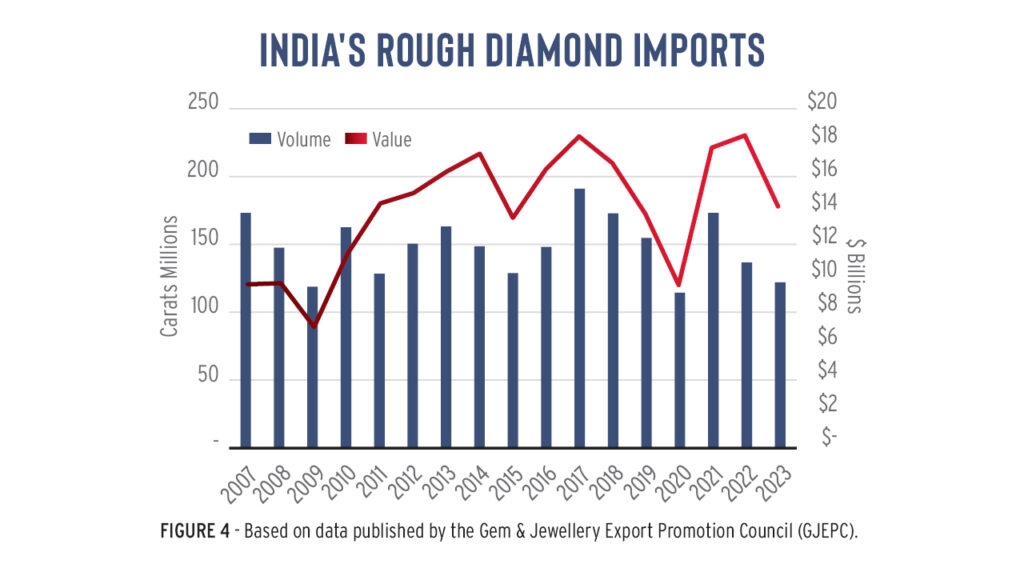

Still, the overall drop in supply reflects the slump in demand that took effect in 2023. Rough imports to India, which accounts for a vast majority of diamond manufacturing, fell 11% by volume and 23% by value, according to data the Gem & Jewellery Export Promotion Council (GJEPC) compiled.

Beginning the year with large inventories, manufacturers bought less rough in 2023. With the entire pipeline overstocked, they weren’t alone. Jewelers, manufacturers and dealers aggressively purchased goods during the post-Covid-19 boom years of 2021 and 2022. They refrained from excess buying as the market slowed.

Sluggish demand

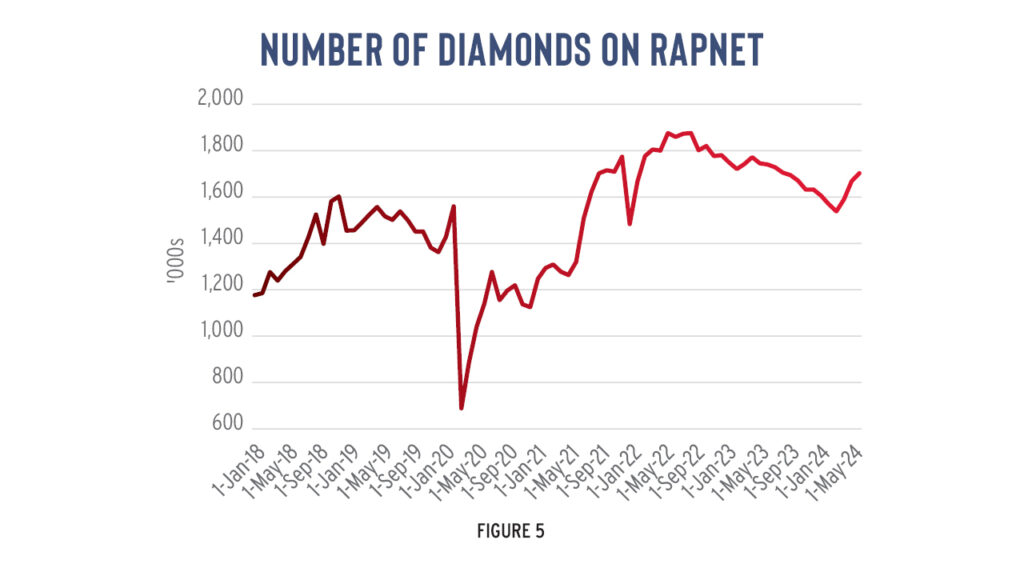

Buyer caution has continued into 2024, particularly while retail demand remains sluggish and manufacturers continue to hold large inventories of polished. The volume of goods listed on RapNet is historically high. As of August, it stood at 4% above levels recorded at the beginning of the year.

Manufacturers are refusing to buy rough, which is why miners are postponing their sales. Unlike in 2023, when production was impacted by Russia’s unique circumstances and operational factors in South Africa, this year the miners are exerting caution due to the weak market.

“Production guidance for 2024 has been revised… as the business responds to the prolonged period of lower demand, higher-than-normal levels of inventory in the midstream, and a focus on working capital,” De Beers explained.

The hope is that supply discipline, combined with an uptick in demand around the holiday season, will help stabilize the market and support prices later in the year, Petra Diamonds stressed.

The miner is right to shift the emphasis to demand. The holiday season will provide a seasonal boost, but the industry has recognized it needs to augment consumer desire for diamonds to solve its supply issues.

U-shaped recovery

Diamond-jewelry retail sales have stagnated.

Chinese consumers are cautious amid the economic slowdown there, while US consumers are feeling the pinch after the sharp increase in the cost of living over the past three years. Only India’s retail space is showing signs of growth and optimism for the industry. Meanwhile, synthetic diamonds have taken market share, translating to approximately $7 billion of lost revenue for the natural-diamond market in 2023, De Beers estimated in a presentation in May.

To fuel demand, De Beers has partnered with Signet Jewelers to promote natural-diamond jewelry in the US ahead of the holiday season. The mining company has an agreement with Chow Tai Fook to do the same in China and has had talks with the GJEPC to raise awareness about natural diamonds in India.

The Natural Diamond Council (NDC) has also launched its “Real. Rare. Responsible.” campaign, highlighting diamonds from the Northwest Territories, which will ramp up through the second half of the year.

Still, current slow market conditions are expected to prevail in the medium term. De Beers CEO Cook stressed on several occasions that this will be a U-shaped recovery, rather than a V-shaped one. Brace yourselves for a prolonged weak market, is the message.

New norms

The mining companies are therefore expected to maintain lower levels of production in the foreseeable future. Besides, several key mines are nearing their end of life. Among those are the Diavik operation in Canada, which is scheduled to halt commercial production in 2026.

Furthermore, several smaller operations have been mothballed due to the downturn. The Renard mine in Canada is the most glaring example of one that could not withstand the slump in demand, but there are several other examples. Meanwhile, very few mines are coming on stream, with Angola earmarked as the most — or only — prospective region for new diamond finds.

With rising costs, the mining companies also prefer to reduce supply than to cut prices, as the value of their sales need to stay above a certain threshold. That is especially true for De Beers, given the scale of its operations and the volume of its supply.

That leaves De Beers — and the rest of the diamond-mining segment — with production to play with, while they hope for an uptick in demand. But it will take a sharp improvement to make those shuttered mines viable again.

It appears that diamond-mining levels are settling at reduced norms. The historic lows evident in the KP data for 2023 set a new benchmark for diamond production. The level will likely be even lower in the current market conditions.

Stay up to date by signing up for our diamond and jewelry industry news and analysis.