The diamond markets are in crisis as we enter a period of great transformation. While it is important to remain optimistic, we must also be realistic and recognize the challenges and opportunities before us. There is a great future ahead for those who embrace change and seize opportunity.

Markets create trade by bringing buyers and sellers together. Quantity and price are determined by customer demand and product supply. Prices and demand are often driven by numerous factors beyond our control, including unknown future events and competition.

In some instances, change is temporary and markets return to a normal, natural, stable equilibrium. In other instances, changes are dynamic and fundamental, creating permanent shifts in demand and supply. New normals are created, and we are forced to change how we do business to stay in business.

Sometimes the forces of change are understood and predictable. For example, the 2021-2023 diamond boom-bust cycle fueled by the economic overstimulation that followed Covid is understood, rationalized and easily predictable.

On the other hand, China’s real-estate-driven economic crisis, intensive cultural shift toward communism, and strong government opposition to conspicuous consumption are just now being integrated into market expectations and prices. It appears that the natural diamond trade can no longer rely on strong Chinese demand.

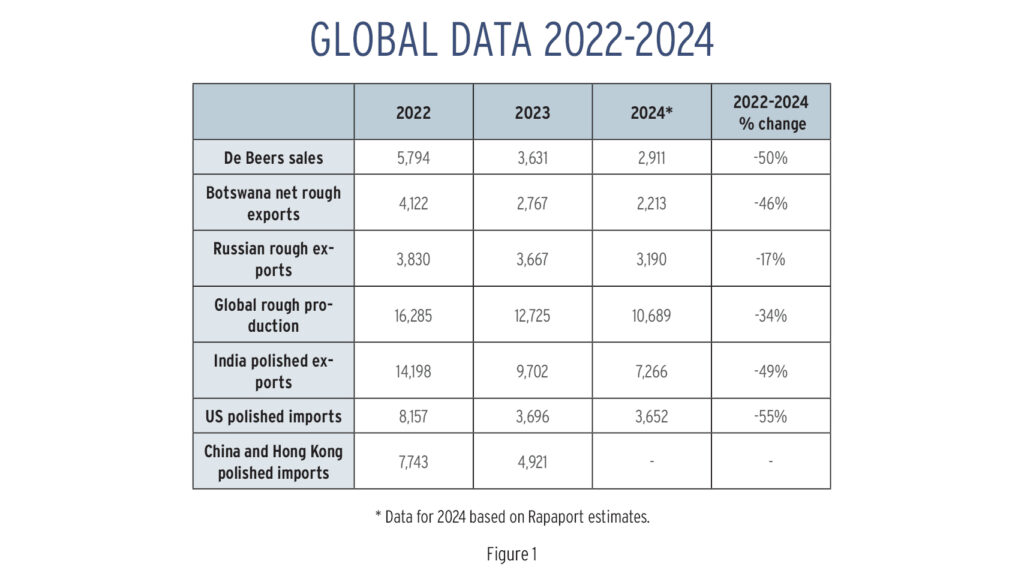

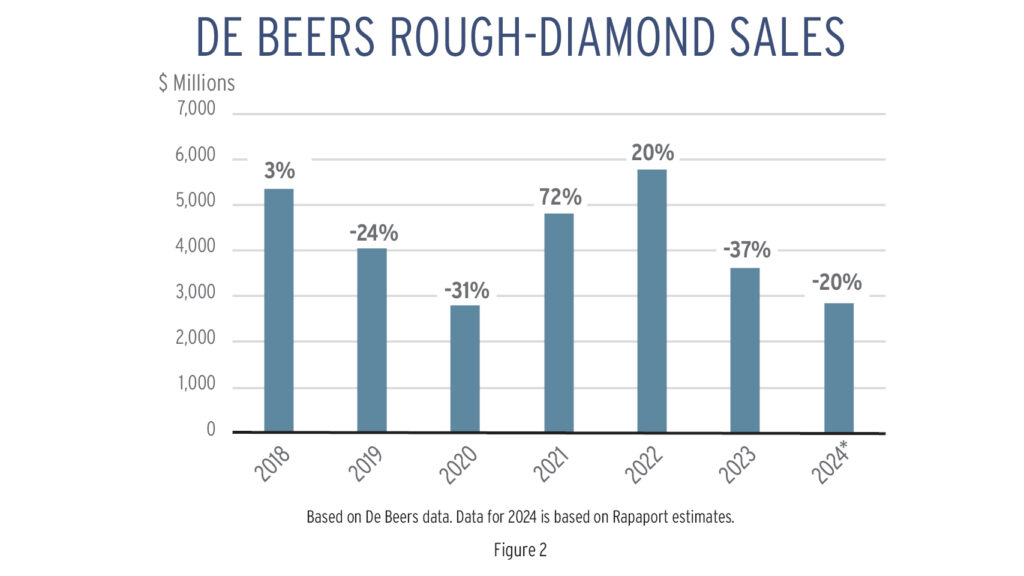

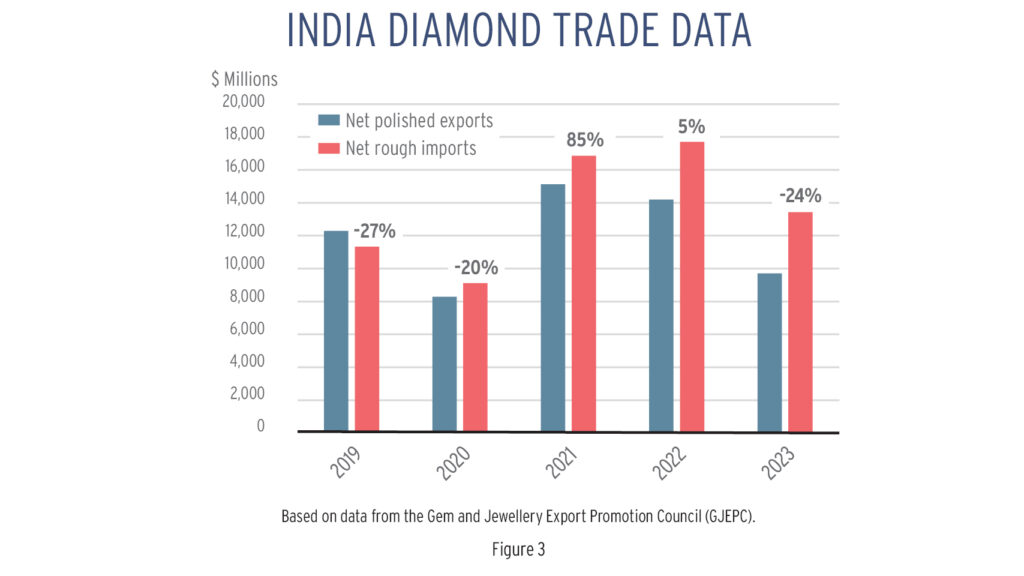

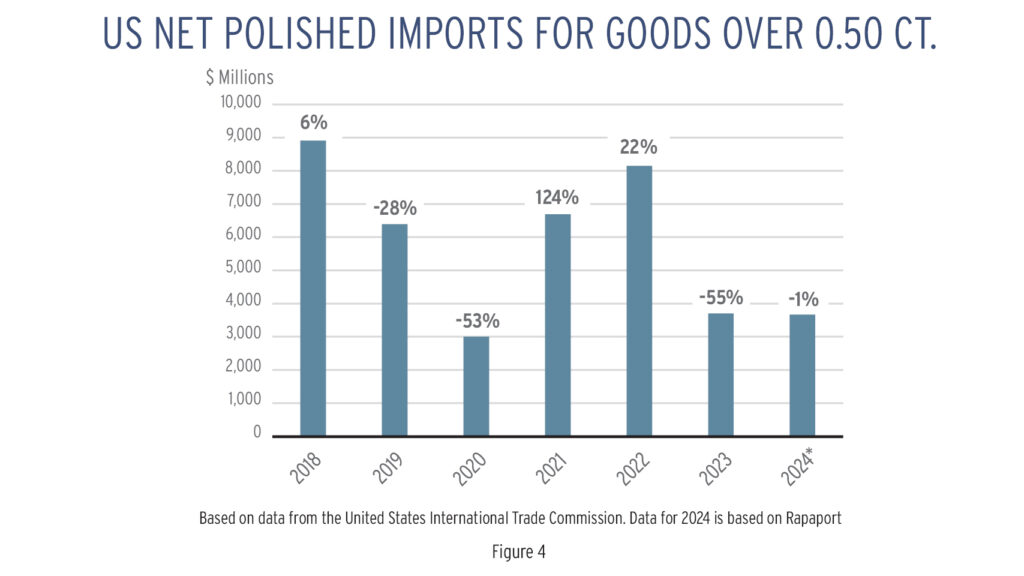

With the advent of strong synthetic-diamond competition, the natural diamond industry has lost approximately 50% of global diamond demand. From 2022 to the end of 2024, we expect De Beers revenue to be down by 50%, India net polished exports down by 49%, and US net polished imports of diamonds over 0.50 carats down 55% (see Figures 1 to 4 on Pages 10 and 11).

Four fundamental forces are impacting the natural diamond markets: 1) China’s decline, 2) India’s prosperity, 3) synthetic competition, and 4) demographics. These forces are interacting in ways that create unprecedented disruption, uncertainty and opportunity.

The slump in China

The decline of China is bound up with a fundamental shift in geopolitics. The forces of globalization that have dominated international trade for decades are now spent, unstable and unsustainable. Trade is being weaponized through sanctions as we enter a new period of global economic warfare.

Trade is not just about money and prosperity anymore. Trade is now about strategic military power and a new world order, with China, Russia and Iran on one side, and America and much of the West on the other side. Countries like India will try to play off both sides, but as the world grows more isolationist and militarized, neutral countries will be forced to take sides.

Free trade is not free. It moves jobs, money, opportunity and power from one country to another. The grand idea of globalization whereby countries operate based on optimization of mutual interests rather than self-interest is over. We should expect a new world order that is much more transactional and much less willing to rely on the goodwill or good intentions of others. The business of nations is now more competitive than cooperative. Friends and enemies are more clearly and carefully defined.

Consider China’s net trade surplus with the US. Between 2010 and 2023, the US accumulated a net trade deficit of $3.9 trillion with China. That is an average of $279 billion per year. If the US keeps giving China billions of dollars of trade surplus every year, the US and its allies will face increasingly difficult national security issues. It won’t just be problems in the South China Sea. China is aggressive and wants to dominate the Far East. It wants to take over Taiwan as it has Hong Kong. It will do so given the opportunity. If the current trade imbalance persists, perhaps China should name its new aircraft carriers or nuclear submarines after those that have paid for them: the SS Walmart and SS Amazon.

The current domestic economic situation in China is also problematic. In spite of the billions of dollars of trade surplus from the US, China is in trouble. The real estate crisis is not going away. Millions of people are not getting the homes they have paid for, the government and its data are not trustworthy, and it looks like unemployment among college-educated youth might be over 40%. The Chinese government is having an impossible time integrating capitalism with authoritarian communism. Without US economic support in the form of trade surplus, China will be in even more trouble.

Recently diamonds with “CTF” laser inscriptions on their girdles have been showing up in Surat. It is likely that some Chinese consumers are selling diamonds to meet financial needs. Another issue is strong Chinese foreign currency controls. If you are a wealthy Chinese person, it has become extremely difficult to send money out of the country. A trip overseas with a few expensive diamonds for sale might solve the problem. As the world gets more controlled, uptight, uncertain and dangerous, diamonds are a good store of value for some. It depends on who you are, where you are and how much money you have. Some wealthy Chinese might be net sellers of expensive diamonds in the months ahead.

Highs and lows in India

India’s dominant position in the diamond trade is evolving. Its 7.5% protectionist import tax on polished diamonds prevents it from being a global diamond trading center. India’s promotion of synthetics has led to the collapse of its natural diamond exports. And Botswana’s added-value beneficiation and source-certification programs will encourage more manufacturing of higher-quality diamonds outside of India.

The good news from India is that it has become the second-largest diamond consumer market. Unfortunately non-Indian companies cannot compete in the Indian market due to their high import taxes.

Since 2000, India has generated a polished-diamond trade surplus of $79.6 billion, with an average $3.1 billion per year. It is outrageous that Indian companies export billions of dollars of polished diamonds to the US while US companies cannot export diamonds to India due to their protectionist tariffs. One wonders who is representing the interests of our US diamond and jewelry trade. Wake up, DMIA, MJSA, and anyone interested in growing their business!

Over the next decade, we expect India to be a major natural-diamond consumer center. Manufacturing activity will decline by about 50% in line with declining natural diamond demand. Production of synthetic diamonds will become highly automated and not provide significant Indian employment.

Supply considerations

For too many years, the focus of the polished-diamond trade has been on mining supply. But mine supply is not the only or best game in town if you want to make money as a diamond dealer, wholesaler or retailer. Diamantaires make more money trading diamonds than manufacturing them. Our focus as an industry must include the opportunities presented by diamonds that consumers want to sell, not just what mining companies want to sell.

As a trade, our allegiance must always be first and foremost to our customers and not to our suppliers. For our customers to trust us and the value of our diamonds, we must buy diamonds back when our customers want to sell. The needs of mining companies and manufacturers are secondary to the needs of our diamond consumers.

Competition from Synthetics

Synthetic diamonds are the greatest short-term threat to the natural diamond business. In 2024, they are expected to account for over 50% of the diamond engagement ring market. We expect synthetic diamonds to dominate the diamond market for low- to middle-income, price-conscious consumers.

We expect synthetic diamonds to replace 50% of consumer demand for natural diamonds. Their impact on the natural diamond engagement ring market and wealthy-class market will lessen in 2025 and over time as synthetic business-to-consumer (B2C) prices decline in line with cubic zirconia, moissanite, and synthetic rubies, emeralds and sapphires.

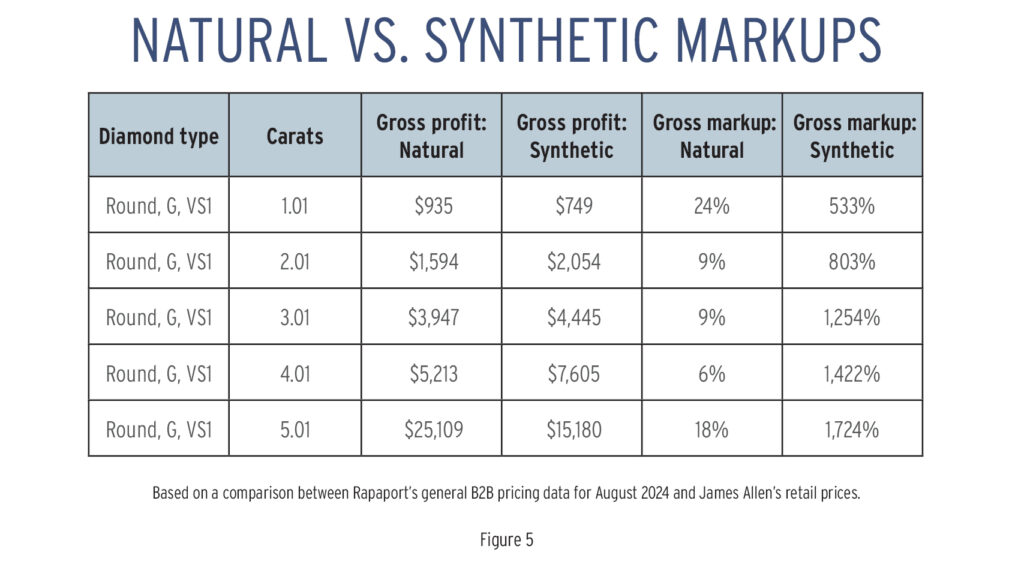

Currently synthetics are providing windfall profits to retailers. In many instances, even at a much lower price point, retailers make more net profit selling synthetics than naturals. While wholesale business-to-business (B2B) synthetic prices have collapsed to hundreds or even tens of dollars per carat, B2C prices have held up, yielding profit margins in the thousands of dollars and percentages (see Figure 5 on Page 11).

Consider a 3-carat, G-color, VS1-clarity synthetic at $4,800 B2C retail. Since the B2B cost is only $355, the gross profit is $4,445, or 1,254%. A natural 3-carat, G VS1 sells for $50,000, yet the jeweler only makes a gross profit of $3,947, or 9%.

Let’s be realistic. If jewelers can make more money selling synthetics at $4,800 than naturals at $50,000, they would have to be crazy to push naturals over synthetics. Jewelers are in business to make money. They have mouths to feed and a business to run. How can you blame a jeweler for selling synthetics?

However, it stands to reason that the windfall B2C profit margins for larger single-stone synthetic engagement rings will collapse by next year. Competition in the retail space will drive down synthetic profit margins to double or even single digits. The net profit margin of most synthetics will fall to hundreds or tens of dollars.

Affordable jewelry houses like Pandora and Swarovski will do exceedingly well providing excellent middle-class affordability, modern design and overall value. Synthetic diamond fashion and women’s self-purchased jewelry will be a big thing next year and in the future.

The battle for the natural diamond market will take place in the diamond engagement ring market. It will not be a zero-sum game. Synthetics will continue to dominate a high percentage of low- to middle-income-level demand for diamond engagement rings, but naturals will begin to assert themselves as a “better” diamond engagement ring and the only kind suitable for the wealthy class. Expensive diamonds will carry great emotional weight for the wealthy and create significant aspirational demand for less expensive natural diamonds.

As more and more Americans get wealthy, natural diamond demand will increase. The fact that someone buys a natural diamond when they could have bought a synthetic says something about them, their status in society, and their level of wealth and sophistication.

It is time for the trade to recognize that diamonds are a very special, expensive and rare product. Synthetic diamonds are for everyone. Natural diamonds are not for everyone. Natural diamonds are exclusive. They are for wealthy people that appreciate their value.

The Great Wealth Transfer

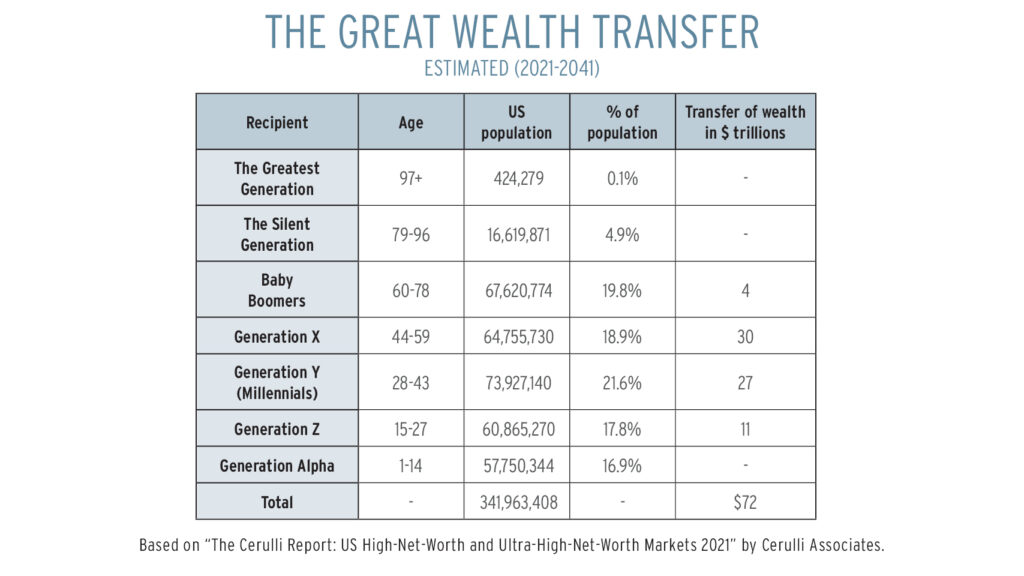

There is a lot of good news coming our way. We are about to witness the greatest transfer of wealth in human history. From 2021 through 2041, younger Americans will be inheriting $72 trillion from older Americans (see table below). That’s $72,000,000,000,000. There are going to be a lot of very wealthy people with a lot of free money they never earned — money that can be spent on valuable diamonds and jewelry.

There are 84 million Americans over the age of 60. Many have fine jewelry that they will be interested in selling. The US market for estate diamonds, gems and jewelry will be booming. It will be a great time to buy jewelry from older people and sell it to younger people who will be getting trillions of “extra” inheritance dollars.

What does the future hold?

The outlook for natural diamonds is good, but only for 50% of the current market. In other words, natural diamonds are going to lose 50% of their market share to synthetics, but the 50% that they don’t lose is going to be very good.

The diamond markets will bifurcate, with natural diamonds being sold to a wealthier class of consumers. Synthetic diamonds will be sold to low- and medium-income consumers who are more budget-conscious. Over time, it is expected that natural diamonds will dominate the diamond engagement ring market due to the low cost of synthetics.

Diamond mining companies will have to work hard to sell their production of less-valuable diamonds, as these stones face high-level competition from synthetics. The benefits of conspicuous consumption will have to be marketed to brides in an acceptable manner, such as the social benefit that source-certified Botswana diamonds bring to the world. The gifting of the natural diamond engagement ring must be combined with the groom’s gifting of social good on behalf of the bride. Grooms must show they have purchased something special for their brides: diamonds that make the world a better place.

This article is from the October-November 2024 issue of Rapaport Magazine. View other articles here.

Stay up to date by signing up for our diamond and jewelry industry news and analysis.