According to an old adage in the diamond industry, success is built on the way you buy, rather than how you sell. In that sense, the biggest challenge for the diamond and jewelry market presents itself during good times. That’s when the industry typically fails to control its urges, overbuying and leaving itself vulnerable during a subsequent downturn.

The diamond and jewelry market currently finds itself in that predicament. Had businesses bought wisely during the strong recovery from Covid-19 in 2021 and the first half of 2022, it would not be facing its current stressful scenario.

The inevitable pullback in the rough market, which is currently in play, typically results from aggressive buying, and mostly at inflated rough prices. This time, the same occurred in the jewelry segment, where retailers bought excessive volumes during the post-Covid-19 period. While we have the benefit of hindsight, both jewelers and manufacturers could have drawn on the experience of previous diamond and jewelry market slumps to adopt a more cautious approach to their inventory management.

Now, as retail sales have slowed, and jewelers have curtailed their orders since mid-2022, the old, familiar pattern has emerged. Manufacturers and dealers are left with excess polished supply, and polished prices have declined.

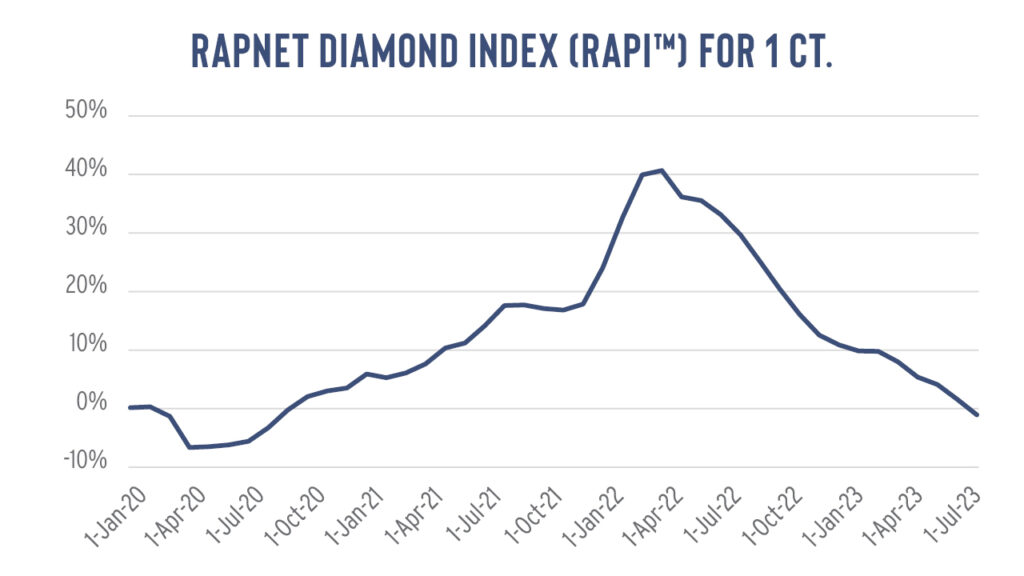

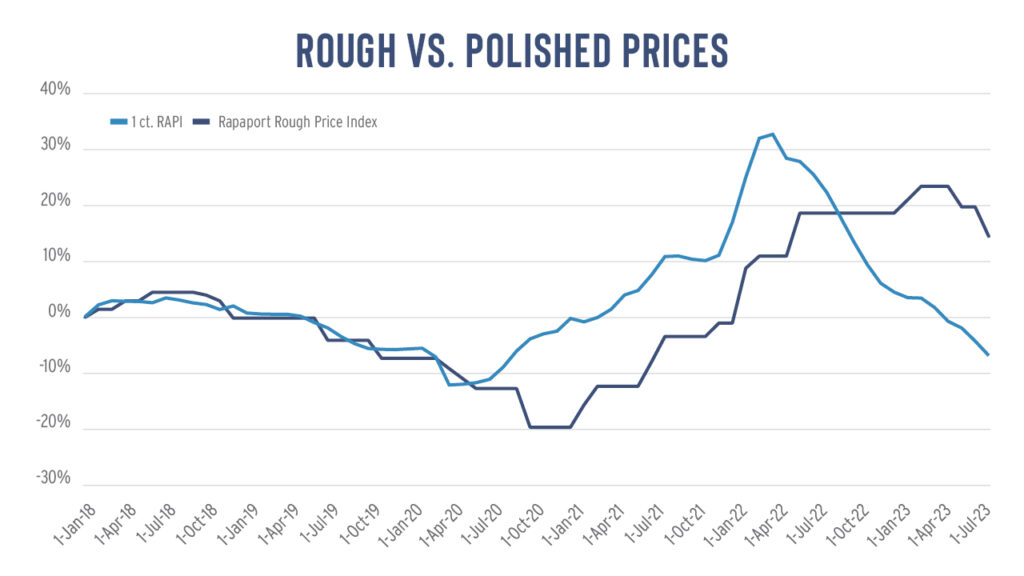

The RapNet Diamond Index (RAPI™) for 1-carat diamonds fell 10.9% in the first seven months of the year, having declined by 10.7% in 2022. The index is now 1.2% below its pre-Covid-19 level recorded on January 1, 2020, having wiped out the gains made during the recovery (see graph).

The RAPI is the average asking price in hundred $/ct. of the 10% best-priced diamonds, for each

of the top 25 quality round diamonds (D-H, IF-VS2, GIA-graded, RapSpec-A3 and better) offered

for sale on RapNet®.

Perhaps the industry could not have foreseen the slump. After all, the slowdown is largely due to US economic prudence, with competition from lab-grown diamonds also playing a part. Rising interest rates and inflation have squeezed consumer savings and spending.

Rising caution

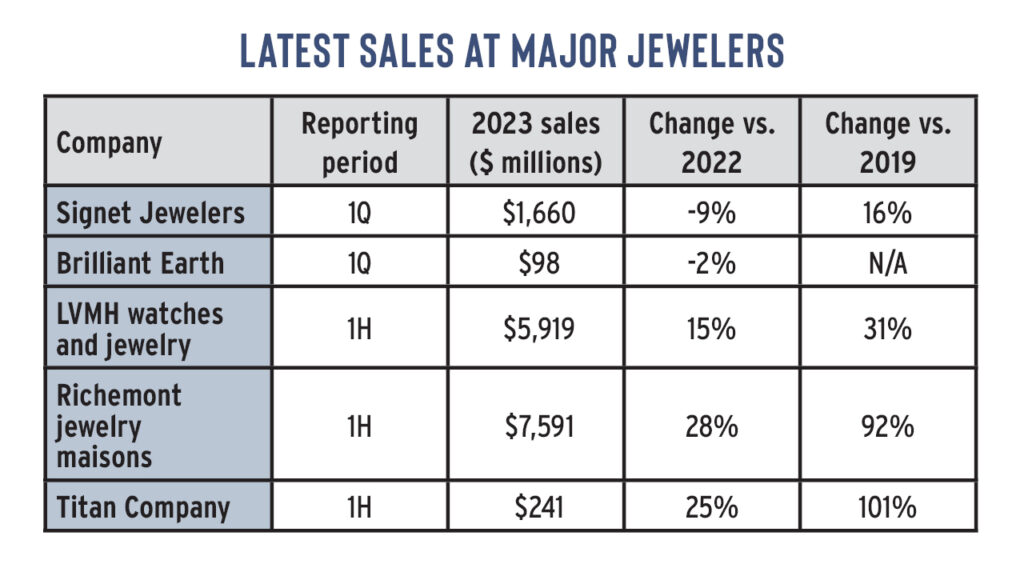

Jewelers have recently expressed greater caution. Signet Jewelers, the sector’s largest specialty retailer in the US, lowered its guidance for the rest of the year, noting “a recent deceleration of trends that have persisted into the second quarter, including a softer than expected Mother’s Day, increasing macroeconomic pressures on consumers at more price points, and deeper competitive discounting,” it said in its first-quarter earnings report published on June 8.

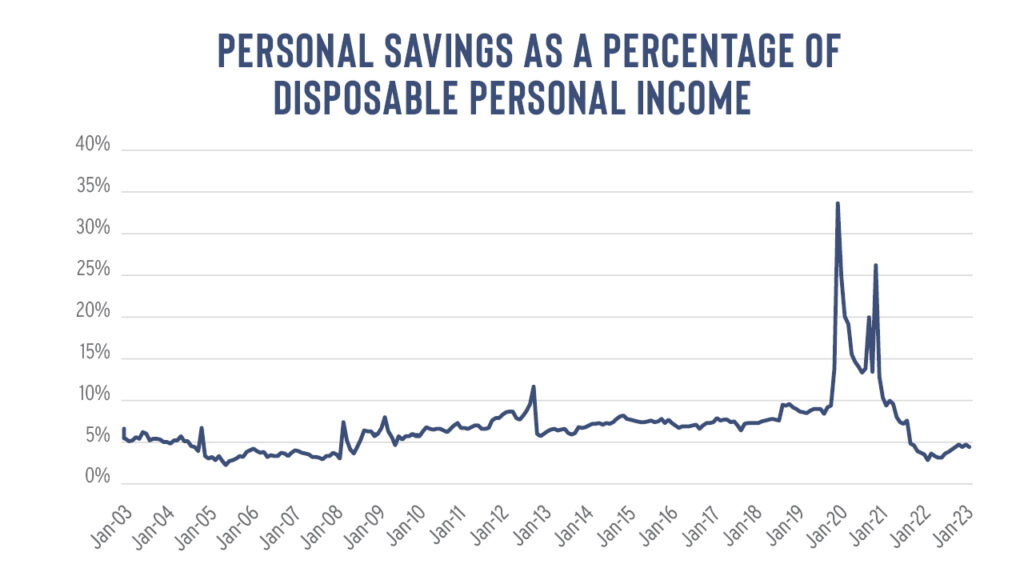

American households have less money available for discretionary spending. Personal savings as a percentage of disposable income slid to 4.3% in June, according to the latest data the US Bureau of Economic Analysis published (see graph). The measure has been at historic lows since the beginning of 2022, after it shot up to 33% during the depths of the pandemic when households spent less on travel and received stimulus checks to see them through the difficult times.

Based on data from the Bureau of Economic Analysis (BEA).

With fuller wallets, there was a release of pent-up demand in 2021 that saw consumers spend more on jewelry and other experiences. The boost in consumer spending encouraged the aggressive inventory replenishment across the diamond and jewelry market pipeline. While consumers overcompensated for what they missed out on during the pandemic, the industry saw the spike in sales as a new normal of higher demand that would be sustained for longer than it was.

Middle America hurting

While retail sales have fallen, they at least remain above 2019 pre-coronavirus levels, driven by strong segments such as the high-end luxury market. But the industry cannot take its current levels for granted. Commercial-quality jewelry sales have declined, that sweet spot that serves Middle America and is most affected by inflation.

Signet reported a slowing in bridal, with group sales down 9% and same-store sales declining 14% during the first fiscal quarter that ended April 29. Signet explained that the inflationary pressure on consumers’ discretionary spending and the expected decline in the bridal category contributed to lower average transaction values. Similarly, Brilliant Earth, which caters to more of a niche market, saw its sales fall 2.3% but a 10% rise in total orders was offset by an 11% decrease in the average order value.

Birks Group, a jewelry chain with stores in Canada and the US, reported 10% lower sales during its fiscal year that ended March 25, adding that heightened inflationary pressures on consumers’ discretionary spending impacted its e-commerce business, which caters to the low- and mid-price-point market.

But there are bright spots at retail. The high end continues to soar, with sales at LVMH’s jewelry and watch division growing 11% and Richemont’s jewelry maisons climbing 19% during the first half of the year. And the major Hong Kong and Indian jewelers have noted a comeback in their respective markets. Chow Tai Fook reported sales rose 29% in the three months that ended June 30.

LVMH and Richemont reported in euros and Titan in Indian rupees, with the numbers converted to US

dollars by the Rapaport Research Report according to the exchange rate at the end of each reporting

period. Brilliant Earth sales data for 1Q 2019 is not available, as its public listing had not occurred yet.

The midstream, meanwhile, is experiencing unprecedented quiet. Jewelers have enough inventory to satisfy their short-term needs, having bought large volumes during the recovery and as they contend with lower sales. But the slump in trading appears to exceed the scope of the retail downturn.

Quiet trading

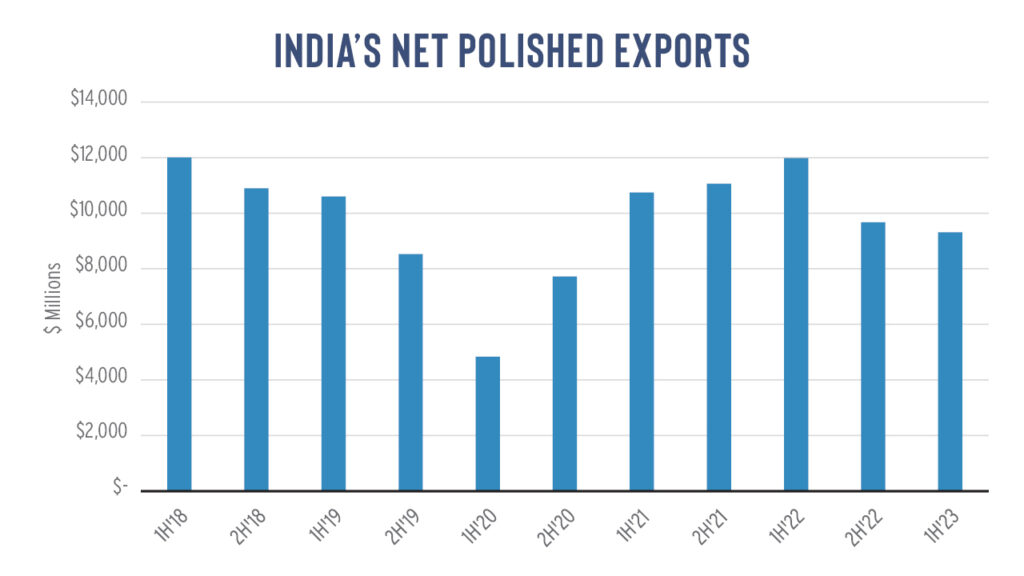

The polished market has declined by a greater margin than the retail segment. India’s polished exports slid 22% year on year in the first half, signaling the extent to which global demand has contracted given its status as the world’s largest manufacturing center and supplier of polished.

Based on data from India’s Gem & Jewellery Export Promotion Council (GJEPC).

Polished-inventory levels remain high. Some 1.75 million stones were listed on RapNet on August 8 — well above pre-Covid-19 numbers, when 1.36 million were recorded on January 1, 2020. Manufacturers have in recent months reduced their polished production to align with the lower demand, and they’ve restrained their rough buying.

India’s rough imports went down 18% to $8.14 billion in the first half of the year, although the volume of its imports was in line with last year. The average price of India’s rough imports fell 18%, signaling a shift to lower quality goods that was likewise described in the retail sector.

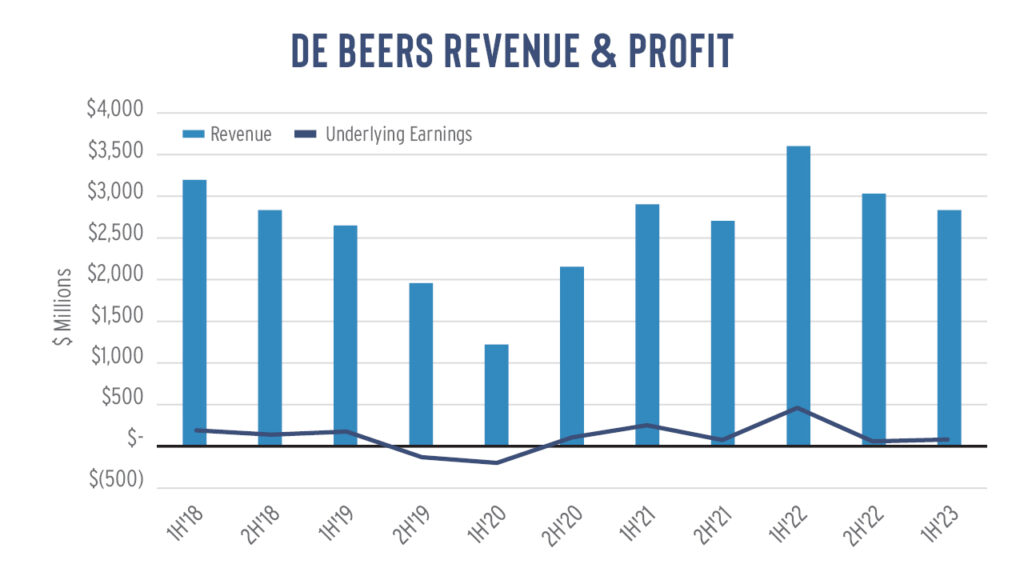

Similarly, De Beers reported a 21% year-on-year drop in first-half rough sales to $2.83 billion, while its sales volume was flat. It sold a higher proportion of lower-value rough diamonds in 2023, it explained. That contributed to a decline in the average price of its rough sales, while De Beers’ average rough price index — measured on a like-for-like basis — fell by just 2% year on year.

Based on Anglo American earnings reports.

Rough prices rallied during the recovery but have not subsequently come down to the same extent as polished. While De Beers reduced prices at the last two sights, it capitalized on the upward-trending market from 2021-2022 for as long as possible, maintaining steady prices even as polished prices were falling. The result is that rough prices remain high relative to polished.

Based on Rapaport estimates and in-house data.

And that is where the trade falls into old habits, with its insatiable appetite for rough when the market is positive and pulling back only when it — along with the mining sector — has no choice but to stop buying. Right now, the market simply cannot incorporate more goods.

A look ahead

So, what lies ahead for the diamond market in this tricky year for the trade? De Beers echoed the sentiment Signet expressed in its market outlook for the second half, saying that “macroeconomic conditions are expected to remain challenging over the near term, impacting consumer spending on diamond jewelry.”

The market is projected to stay quiet through the remainder of 2023. Much will again hinge on the holiday season as prospects for 2024 appear more positive, with stabilized interest rates and normalized inflation.

In the meantime, jewelers, manufacturers, and miners will be cautious in their inventory management, as the market gradually regains its balance between supply and demand. The focus must be to stimulate demand to enable a return to an upward trajectory in 2024 — perhaps back to the new normal of higher sales that the recovery from Covid-19 promised. And when that does happen, the diamond and jewelry trade might be more prudent in the way it buys, lest it suffer another down cycle.

This article first appeared in the August edition of the Rapaport Research Report. Subscribe here.

Main image designed by David Polak.