De Beers is embroiled in momentous negotiations with the Botswana government that are threatening to derail their model partnership. For the first time in their 54-year relationship, the two are simultaneously in talks for a new 10-year marketing deal as well as the 25-year license governing their Debswana mining joint venture.

Naturally, the marketing agreement has garnered more attention as it facilitates the country’s beneficiation program — the process of adding value to its mining operations by enabling services further along the supply chain such as manufacturing and trading. It’s also the area that appears to present more wiggle room for De Beers.

In a politically charged environment, in which diamonds are responsible for such a large part of the country’s economic welfare, it may be easy to perceive the company as taking a disproportionate part of the country’s sales.

Botswana reportedly wants to raise its share of the pie. President Mokgweetsi Masisi was quoted as saying the government wants a higher percentage of the local output for its own sales, and that the government was prepared to walk away from the talks if its demands weren’t met.

The exact nature of its conditions has not been disclosed. It is likely they revolve around the share of production that goes to Okavango Diamond Company (ODC) — the parastatal that conducts rough sales on behalf of the government. The distribution of specials, large diamonds above 10.8 carats, may also be on the table, as might be how the sales take place and the percentage of De Beers rough supplied to Botswana-based factories.

Mining Leverage

Whereas the government appears to have some bargaining power when it comes to the pending marketing agreement, De Beers holds the cards with regard to the mining one. And diamond mining carries more weight than sales when it comes to Botswana’s fiscal strength.

Consider that an estimated 80.8 cents from every dollar generated by De Beers mining operations in Botswana goes to the government in the form of royalties, taxes, and dividends. In terms of gross domestic product (GDP), mining makes the biggest contribution of any sector, accounting for some 20% of the total, of which diamond production makes up the vast majority.

Mining is where De Beers has its strongest influence in these talks. The company invests enormous amounts to ensure production continues, largely through majority shareholder Anglo American, and it has the technical know-how and experience to manage projects of such a scale.

As De Beers cochairman Bruce Cleaver explained recently on the Rapaport Diamond Podcast, decisions need to be made on major expansion projects that are due at the Jwaneng and Orapa mines. De Beers cannot make such investments — which could amount to billions of dollars — without the mining licenses in place, he stressed.

While the marketing agreement and mining license have historically been signed independently of one another, this time they connect the interests of both parties, suggesting one might be used as leverage to influence the other.

Complex Ownership

It is therefore no simple matter for either party to walk away if their demands aren’t met. And perhaps in that context it is understandable the agreement has been postponed three times already. But there is some expectation that the June deadline must be the final one.

If so, it is difficult to consider a worst-case scenario in which a deal is not reached and what that would mean for the broader relationship between De Beers and the Botswana government. Their partnership and ownership structure are already complex, adding an extra layer of complication to the negotiations.

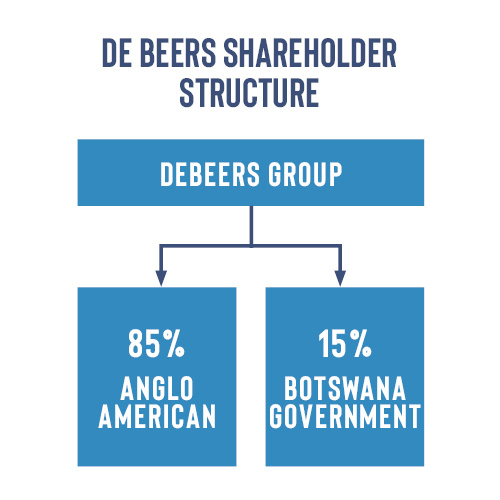

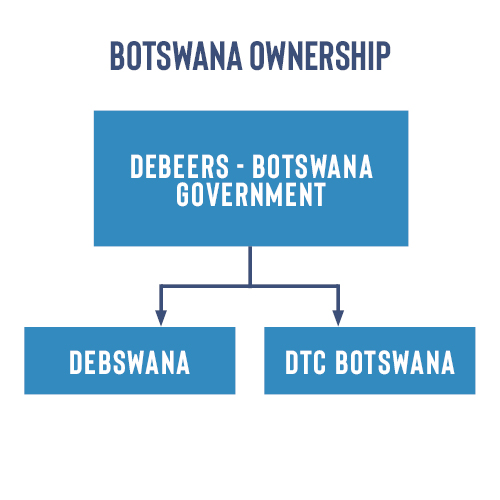

Botswana owns a 15% stake in De Beers Group, with Anglo American holding the remaining 85%. The government and De Beers are also equal joint owners in Debswana, which oversees De Beers’ Botswana mines, as well as in Diamond Trading Company Botswana (DTCB), which sorts and values that production.

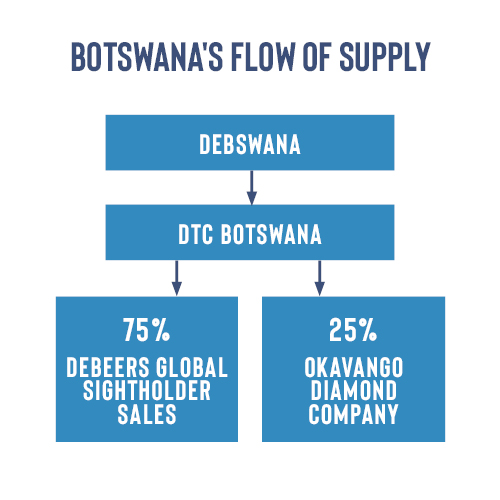

Essentially, production from Debswana’s four mines — Jwaneng, Orapa, Damtshaa and Letlhakane — is sold to DTCB where it is sorted and valued for distribution to its two clients: 75% going to De Beers Global Sightholder Sales (GSS) and 25% to Okavango under the current arrangement. At GSS, the DTCB goods are mixed with production from other De Beers mines in Canada, Namibia and South Africa and aggregated into categories for distribution to sightholders.

Given that complex ownership structure, what would it mean for GSS if a marketing deal were not reached? After all, GSS relies on DTCB and therefore also on Debswana for two-thirds of its supply, playing a key role in helping De Beers meet its long-term commitments to sightholders.

The government has an interest in GSS’s success too. It earns dividends from DTCB’s sales to GSS and, as a 15% owner of De Beers, would be compromising its potential revenue there. Furthermore, GSS employs 234 people, of which 220 are Batswana, and reducing GSS activity would put their jobs on the line.

The Okavango Factor

And what would failure to sign an amicable marketing agreement mean for half-government owned Debswana and DTCB? That production could arguably go to Okavango. But does Okavango have the capacity to handle such large volumes?

Okavango sells via auctions held 10 times a year, coinciding with the De Beers sights. It sold an estimated 5.9 million carats for $1.27 billion in 2022, according to Rapaport calculations. Yet auctions are volatile and dependent on market conditions. The De Beers sight system, with its long-term contracts, offers greater stability and protection from a downturn, thus giving some assurances for stable revenue to DTCB that Okavango currently cannot provide.

Okavango doesn’t have the capacity to implement a sight system. But the government’s deal with HB Antwerp announced in late March might provide an interesting alternative. The government intends to acquire a 24% stake in HB Antwerp and supply the manufacturer with rough through Okavango. No further details were disclosed, such as how much of Okavango’s supply will go to HB Antwerp — whether it will be all, a percentage of its run of mine, or just the specials.

Viewing itself as a disrupter, HB Antwerp is looking to replicate with Okavango its arrangement with Lucara Diamond Corporation, the owner of the Karowe mine in Botswana. HB Antwerp has the exclusive rights to all of Lucara’s specials, through which Lucara gains a profit share from the sale of the resulting polished stones by the Belgian company.

HB Scaling Up

The government has taken note of that agreement, while strengthening its ties to Lucara through the Karowe operation, and to HB Antwerp, which in late March opened a state-of-the-art factory in Gaborone. At the very least, it seems to want to sell Okavango’s specials through HB Antwerp, in a similar way that Lucara does.

For its part, HB Antwerp plans to ramp up its Botswana operations. Its new facility is “the most advanced diamond facility in the world,” claimed cofounder and managing partner Rafael Papismedov in his speech at the opening. And the company is currently breaking ground on a second factory there, “an even more ambitious plan that is 15 times the size,” he added.

HB Botswana, as the local subsidiary is known, has committed to scale up its business in Botswana by as much as 10 times in the coming years, growing to 485 employees by 2026, from the 30 it currently employs, President Masisi said at the factory inauguration.

For HB Botswana to operate at such scale, it will need more than just Okavango’s specials. It will require a fair share of Okavango’s run-of-mine commercial goods as well, with a promise to add value on those goods too.

Perhaps Lucara can play a role there. Lucara is looking for third-party suppliers to sell rough through its Clara platform, which it claims is an innovative way to market goods according to the buyers’ polishing needs. While Clara has been a slow burn for the company, Lucara still claims that diamonds sold through the system gain a premium.

While HB Botswana clearly plans to increase its manufacturing of rough to polished in Gaborone, it may have excess rough, through its deal with Okavango, to sell through Clara. A speculative scenario in which Okavango supplies HB Botswana its run-of-mine supply, and HB Botswana places a portion of the non-specials from Okavango on Clara, while the Belgian company sells the specials of both Okavango and Lucara, might not be farfetched. At press time, Lucara did not reply to a request for comment on whether it was in talks with the government or HB Antwerp for such an arrangement.

De Beers’ Bargain Chip

Given the scale of its production, De Beers cannot offer the government a profit-sharing arrangement. Such a deal is manageable for Lucara given that it has one mine, with relatively small production of 335,769 carats in 2022, and one client to sell its specials to — HB Antwerp. De Beers produced 34.6 million carats in 2022 and has long-term sales contracts with some 80 sightholder clients with whom it would be difficult to involve in any profit-sharing deals.

All De Beers can do is offer Okavango a greater share of DTCB supply: Perhaps it could raise it from 25% to 30%, or 40% at a stretch. Debswana’s 2022 production reached 24.1 million carats and had an average sales price of $193 per carat, according to Anglo American’s annual report. Every 5% increment of that amounts to 1.2 million carats valued at around $232 million.

Another negotiation point could be on the split of Debswana/DTCB’s specials of 10.8 carats and above. Under the current arrangement, these higher value goods are sold to De Beers GSS and Okavango in the same 75-25 split as are the rest of the goods. Perhaps the government would be content to keep those proportions in place for the run-of-mine goods but raise Okavango’s share of the specials?

Either way, is De Beers willing to depart with such volumes, and can it afford to? After all, it has commitments to provide consistent supply to sightholders, and it relies heavily on Debswana and DTCB to meet those demands.

Taxing Issues

The government might also be pushing De Beers for clarity on an alleged tax dispute relating to its moving GSS from London to Gaborone in 2013.

As a De Beers spokesperson explained: When De Beers agreed to set up GSS in Botswana, it was effectively transferring part of its UK business to Botswana, including the revenue from the sale of rough diamonds to sightholders. However, the UK business continued to undertake functions which were critical to the success of the diamond industry such as synthetic research, the development of synthetic development technologies as well as creating and delivering a marketing strategy. The cost of these activities beneficial to the functions of GSS are covered by intercompany transactions – a marketing charge and royalty of 2% of total rough sales that GSS pays to De Beers UK.

A leaked report from the Botswana Unified Revenue Service (BURS) contends that De Beers management knowingly presented “unreasonable, unrealistic, dishonest, baseless and misleading” forecasts to the government and tax authority to justify the royalty, the local press published in January. The report claims that between 2013 and 2020, De Beers made gross profits of as much as $1.35 billion from GSS through royalty, marketing, and research and development fees charged by De Beers UK.

In response to the allegations, De Beers contended there were periods when the trading business was in fact unprofitable during the reported timeframe. The company could not foresee in its initial projections the market downturns of 2015 and 2019 that led to significant operating losses. The spokesperson further stressed the contribution De Beers had made to the country’s fiscus.

“Despite De Beers making no profit globally from diamond trading activities between 2013 and 2020, our Botswana-based diamond trading business still paid billions of pula in taxes in this period… [and] far greater tax contributions have also been delivered by the Debswana diamond mining joint venture,” the spokesperson stressed. “During the most challenging economic periods, De Beers has continued to purchase rough diamonds in Botswana, supporting Debswana and the economy even when such activity is unprofitable, and continued to invest in consumer marketing to support the long-term value of the industry.”

“We are committed to ensuring we pay the right amount of tax at the right time, and we engage with BURS in an open, transparent and constructive manner to ensure this is the case,” he added.

Balancing Needs

Still, the miner might make some concessions on this issue as the negotiations reach their climax — perhaps reducing the royalty paid to the UK business moving forward.

But the Botswana government will also need to soften its stance. In speaking to officials on condition of anonymity, one sensed there’s a split within government circles on how to approach the final talks. There are those who understand and value the long-term relationship with De Beers, while others are pushing for change, fueling the perception that Botswana has got a raw deal from the company.

The result may be a compromise between the two.

The government ought to recognize the tremendous contribution De Beers has made – and can continue to make – in the country. As President Masisi noted, today there are 48 cutting and polishing companies operating in Botswana, with employment in the sector nearly doubling in the past year to 4,001 workers as of January 15, 2023.

He might be reminded that none of that would have been possible without the contribution of De Beers. While a fresh approach may be needed on the sales side, Botswana needs to incentivize De Beers to invest in the country’s mining operations and maintain the strong trading presence that has inspired growth of Botswana’s manufacturing sector.

De Beers, meanwhile, will walk a fine line between protecting its heritage in the country and bringing innovation not only in mining, but facilitating new added value for Botswana in its sales mechanisms, too – especially as others are tempting the government with a shiny new business model.

A Precedent Set

There was an air of uncertainty and excitement on the summer day in November 2013 when sightholders arrived in Gaborone for the inaugural De Beers sight in the city. The historic occasion broke the tradition spanning more than 70 years of holding the sales in London.

Some in the industry bemoaned the move, as attending sights at De Beers’ headquarters on Charterhouse Street brought a certain prestige to which they clung. There were also practical concerns, with the lack of direct flights to Gaborone meaning a longer commute through Johannesburg, South Africa, while the city also lacked London’s hotel and restaurant riches.

But De Beers had to make the move. It was completely invested in beneficiation in Botswana, with the country seeking to diversify its economy and reduce its reliance on mining. As per its 2011 marketing agreement with the Botswana government, the company had already moved its aggregation and sorting operations to Gaborone, siphoned more rough for manufacturing in the country, and given up 10% of Botswana production so that the government could conduct independent sales through the newly established Okavango Diamond Company. Okavango’s share grew to 15% after five years, as per the agreement. It rose to 25% when the contract expired in 2021.

Indeed, the 2011 marketing agreement was a gamechanger for Botswana. In the decade since its signing, Gaborone has established itself as a major rough-trading hub and polishing center, empowering thousands of Batswana in various diamond-related skill sets, while the government-owned Okavango has become a major supplier of rough.

De Beers also benefited. Its presence in Botswana laid the foundation for its Building Forever program and is a symbol of its positive corporate governance.

That agreement was a win-win, despite the perceived sacrifices De Beers made. It was hailed as another example of the exemplary relationship between De Beers and Botswana — a model of effective corporate-government partnership.

Replicating the impact of that deal was always going to be a challenge in the current round of negotiations. How could the parties again bring about such massive change to the benefit of all involved? That seems to be a sticking point as De Beers and the Botswana government hope the new deal, too, will have a lasting effect on both country and company.

This article first appeared in the March edition of the Rapaport Research Report. Subscribe here.

Main image: david polak/midjourney