At the beginning of the 21st century, the diamond industry operated as a perfect example of globalization: It mined rough in Africa, sold it in London, cut it in Surat, and retailed the resulting goods in New York — a smooth, efficient international supply chain. Yet as we stand at the beginning of 2026, the diamond world is smooth no longer; it is mountainous, fragmented and walled in by tariffs and sanctions — all against a backdrop of ongoing geopolitical friction and shifting consumer preferences.

This article examines the complex dynamics of the past year, which saw the rules of the game written in Washington boardrooms and in synthetic-diamond factories. Aside from the US tariffs on Indian goods and a tightening of sanctions on Russian-origin diamonds, the polished market split into three segments, each one its own economic world (see table below). Meanwhile, efforts to meet consumers’ fancy-shape demands collided with the physical constraints of the rough, which led to both shortages of quality goods and an oversupply of less-desirable ones.

Geopolitical upheaval

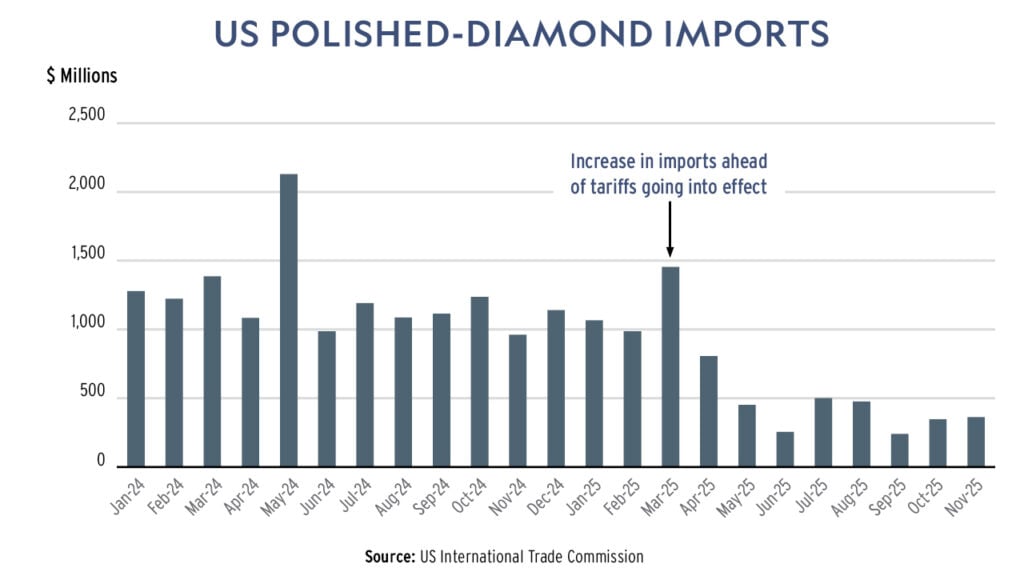

The most disruptive and dominant event of 2025 was the escalation of the US-India trade war. What began as a threat became reality when the Trump administration imposed reciprocal import tariffs of 25% on Indian products, then raised them swiftly to 50%. The latter move — which originally aimed to punish India for buying Russian oil — turned an already troubling development into an existential crisis for the diamond industry.

The tariffs struck deep into supply lines, led to a dramatic fall in US polished imports, and affected inventory in both America and India, creating bubbles in some categories and shortages in others. As a result, the gap between the two nations’ polished prices widened, with 1-carat commercial goods becoming 18% more expensive in the US than in India.

The crisis hit hardest in the manufacturing hub of Surat, which cuts some 90% of the world’s natural diamonds. With the US — a market that accounts for close to half of global demand — erecting tariff walls this high, Indian manufacturers reduced their rough purchases and their factory output to avoid accumulating polished inventory they wouldn’t be able to export to this primary destination. While larger manufacturers are surviving the resulting upheaval, press reports have documented widespread layoffs and the closure of small and mid-size factories.

All of this took place under a heavy fog of uncertainty. The first half of 2025 was characterized by a lack of clarity about these tariffs and their rates. In the second half, the uncertainty stemmed from the ongoing negotiations between the countries and from US courtroom debates about whether the tariffs were legal to begin with.

The market responded by making strategic attempts to alter course — to reroute supply chains and redirect production to alternative centers, particularly Antwerp, which had secured a 0% tariff rate.

The US and India later reached a deal to drop the oil penalty and reduce the reciprocal tariffs to 18%. The February 2026 agreement was expected to abolish all duties on Indian gemstones and natural diamonds once finalized, with finished jewelry and lab-grown diamonds retaining the 18% rate. However, uncertainty returned after the US Supreme Court ruled that Trump’s tariffs were invalid. It remains to be seen how these developments will influence the market.

The synthetic threat

In 2025, it became clear that synthetic diamonds were here to stay — and that they were destroying volume and value in the natural market.

Miners and manufacturers failed to adjust their output to match the falling demand for natural diamonds, and the resulting high volumes of natural goods pushed prices downward. Meanwhile, buyers were becoming more selective about the quality of their diamonds, seeking stones without black centers or other noticeable flaws. This hyperfocus on specific natural goods — especially with the flawlessness of synthetics for comparison — became an acute problem, leading to inventories of diamonds that were hard to move.

In the fancy-shape segment, synthetics set the standard for proportions and brilliance, causing even greater consumer selectivity. Even if a jeweler succeeded in convincing a client to purchase, say, a natural oval, the consumer would demand that the brilliance and proportions be at least identical to the synthetic equivalent.

Large corporations and chains with sufficient sales volume to sustain a business model of low profits per unit gained a clear competitive advantage over independent jewelers in the synthetic-diamond niche. The independents began to abandon the category and to focus on natural diamonds. However, this created a misleading picture: By mid-2025, it appeared as though the drift toward lab-grown diamonds had halted, when in reality, the demand had simply shifted from independent jewelers to the large chains.

The rough sector: From seller’s to buyer’s market

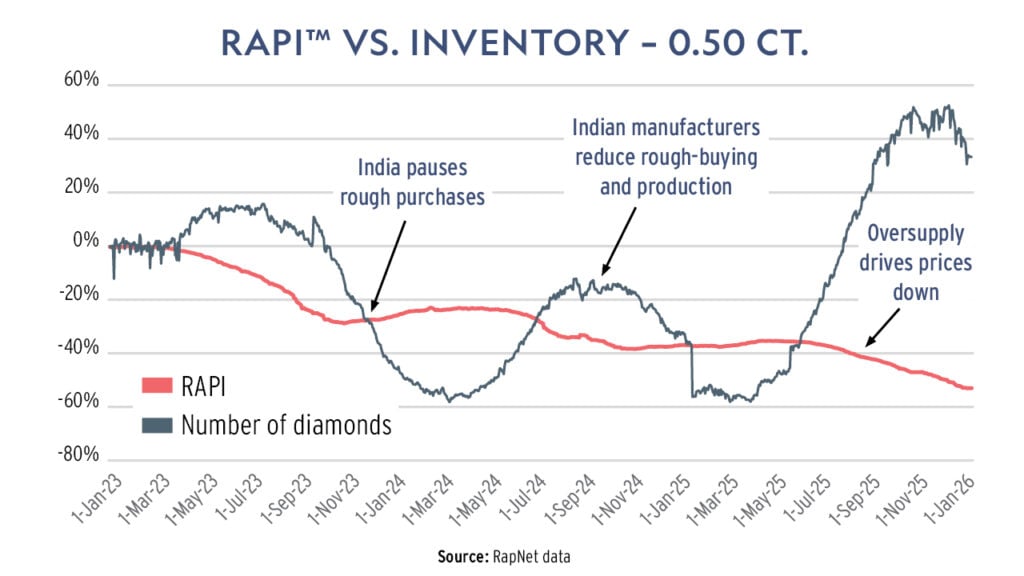

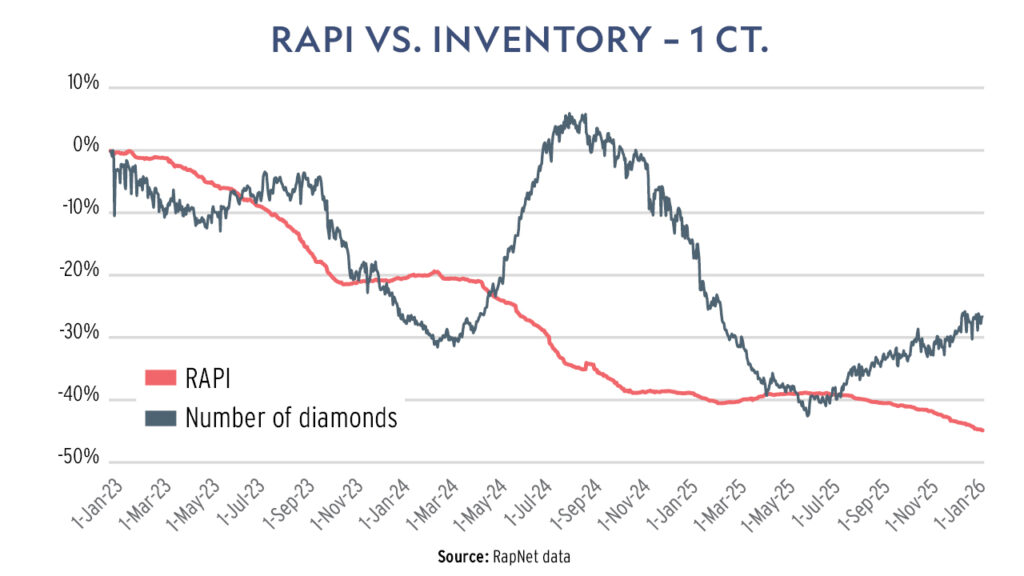

Far-reaching changes occurred last year in the rough market. In previous years, it had been a seller’s market: The mines dictated the terms, and manufacturers had limited room to negotiate. However, the 2025 market favored the buyer when it came to rough below 3 carats. In these sizes, goods sold at cheaper prices, or at least on better terms that amounted to the same thing. Manufacturers who bought cheaply were able to offer polished at competitive prices, and this cycle accelerated the price declines in polished goods.

Rough also continued to sell through the tender method. While this is an efficient way for miners to sell off their inventory, it has its downsides: In such a weak market, the prices achievable through tenders are lower than those of allocation sales like De Beers sights.

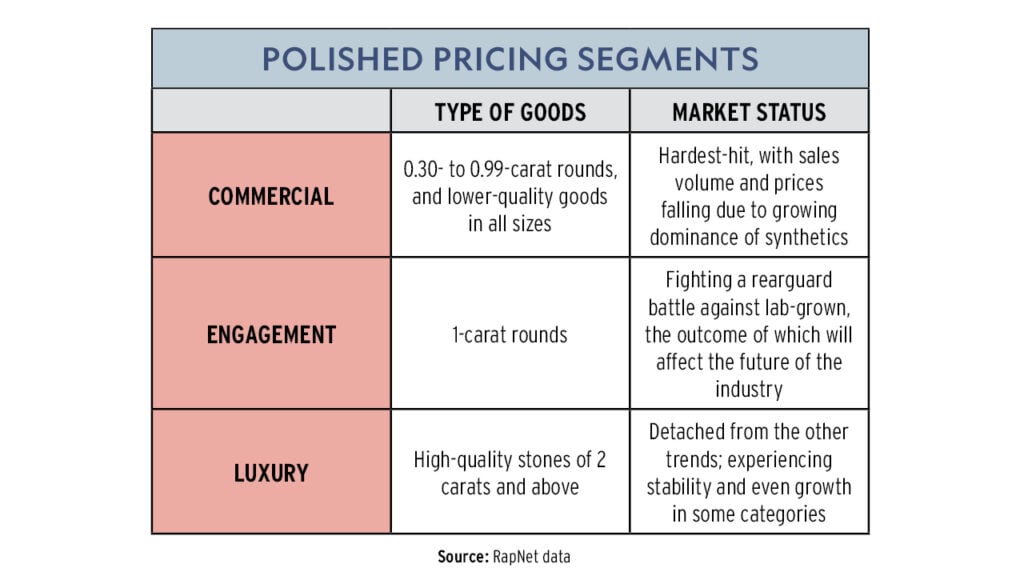

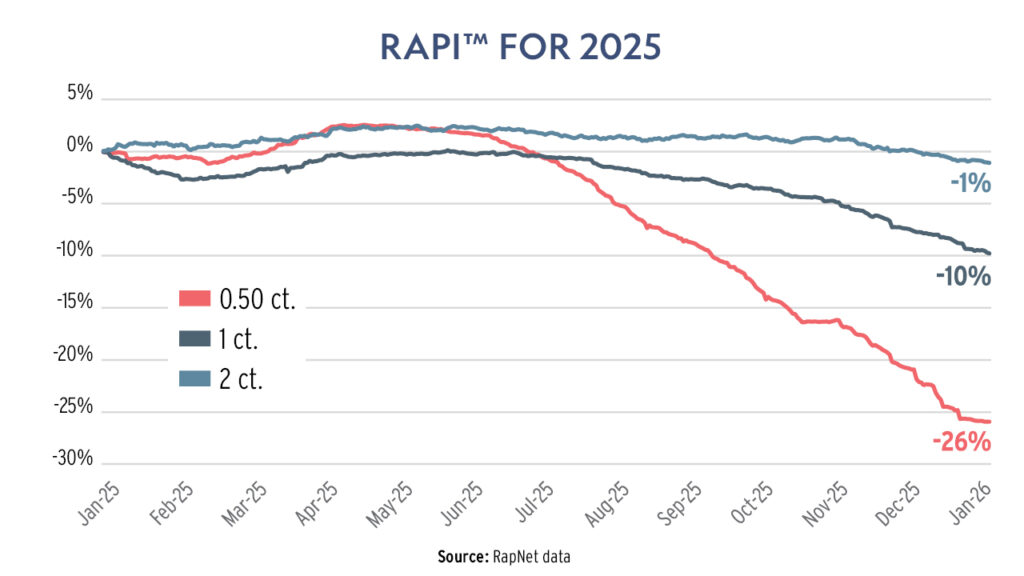

Prices: A three-way split

Diamond prices were relatively stable in the first half of 2025, though they also reflected the fragmentation of the polished market into three separate categories, each behaving completely differently.

The commercial segment saw heavy losses. Round diamonds of 0.30 to 0.99 carats and lower-quality diamonds of all sizes — such as those with inclusions visible to the naked eye — lost customers who preferred to buy a synthetic diamond over a natural one. This led to a fall in prices. A combination of near-zero diamond imports in China and a tough struggle with synthetics in the rest of the world led to historically high inventories in the 0.30- to 0.69-carat range, which pushed the price down even further. Diamonds between 0.01 and 0.17 carats had maintained relative price stability in years prior, but in the second half of 2025, they declined significantly in value due to tough competition with synthetic diamonds, which until recently were less dominant in these sizes.

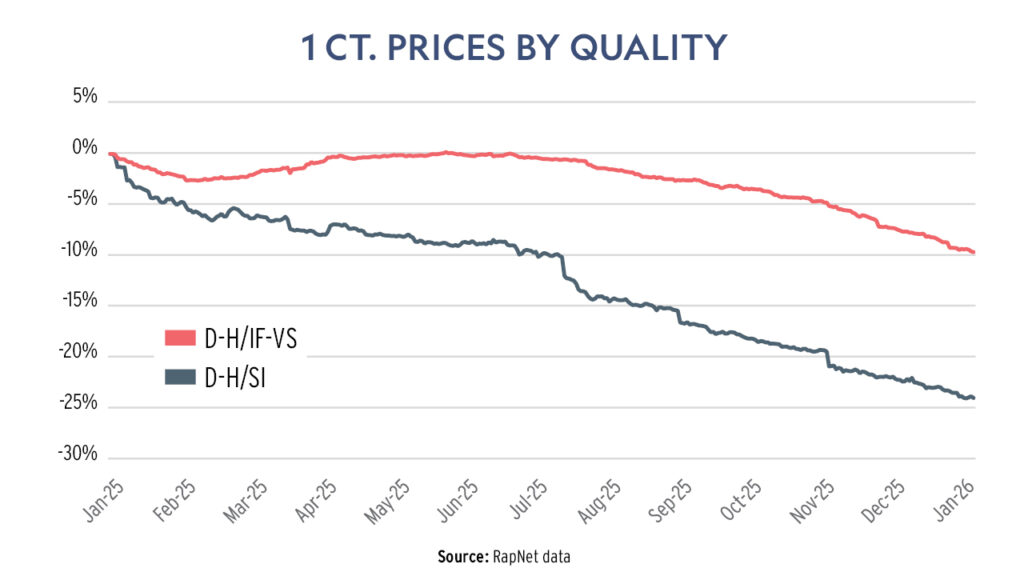

In the engagement segment — mainly 1-carat rounds — natural diamonds are waging a defensive battle against synthetics. Lower-quality natural stones, such as those that aren’t eye-clean or that have a central black inclusion, suffer from a lack of demand. Engagement customers want diamonds that are beautiful and visually perfect, or they will opt for a synthetic stone.

Meanwhile, the luxury segment — 2 carats and above — saw stable pricing. This market demands high standards, so diamonds of good quality and excellent proportions performed well. For luxury customers and budgets, synthetic diamonds are not a worthy alternative, so this segment operates in an entirely different manner from the commercial and engagement ones.

Attempts to apply a single approach to these different markets will not succeed.

Fancy shapes: Going long

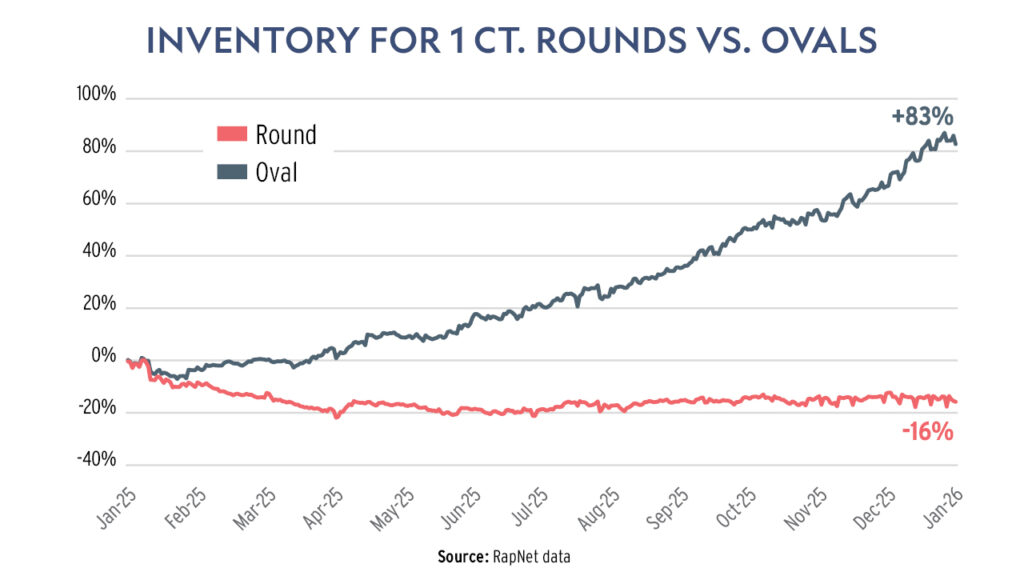

At the product level, 2025 was without a doubt the year of fancy shapes. The classic round diamond — which still dominates in terms of volume — lost significant market share in the premium segment to elongated fancy cuts.

Demand for the marquise in particular saw a surge; it’s currently the most expensive shape, reflecting low availability. The oval continued to be the most popular fancy shape, along with the cushion and the elongated radiant.

Many buyers began to demand a minimum length in millimeters for various sizes in oval and pear. (The Gemological Institute of America (GIA) has yet to set official parameters for cut grades in the fancy-shape category, something the industry has long been awaiting.)

Manufacturers responded to these trends and shifted production from round to oval. However, they ultimately exceeded demand, and a portion of the ovals they produced — the ones from suboptimal rough — were too short to satisfy consumer preferences. The result was a rise in oval inventory and a softening of prices.

Goods of 2 carats and above in elongated fancies were the hottest items throughout 2025, with demand surpassing supply and creating upward price pressure in specific categories.

Insights: What next?

Uncertainty is the new norm. The industry needs to build business models that assume uncertainty as a baseline and not as an anomaly that will pass. Moreover, companies need to try and turn that uncertainty from a bug into a feature — to leverage it into a competitive advantage.

How? Through a deep understanding of the problems uncertainty causes for customers and competitors. The businesses that manage to function best under these conditions will gain a meaningful advantage.

De Beers no longer constitutes a stable and transparent supplier of rough; its future is up in the air as parent company Anglo American seeks to sell it off, and there’s no guarantee the new owners will maintain its current supply method. As such, many companies are recalculating their strategies, considering not only how to obtain a reliable flow of goods, but whether it’s worth their while to remain in this industry at all.

The fragmentation of the trade by location, size and shape poses another enormous challenge for all diamond dealers. American branches of Indian manufacturers are competing with more established offices there. Producers are struggling to meet the high demand for long fancy shapes and to manage the high inventories and reduced prices that resulted from their attempts to increase oval output.

The oversupply issue — which also extends to small commercial goods and the categories under threat from synthetics — has created an excessive burden on manufacturers. When buyers know there are always more goods and someone willing to sell for less, they will wait until the last moment to make a purchase. However, cutting production of smaller and less-desirable goods to reduce the surplus can lead to a low supply of larger sizes and sought-after goods as well.

The industry needs strong leadership to break this cycle and restore a balance between supply and demand. Among other things, that means stimulating the public appetite for natural diamonds by investing heavily in quality generic advertising — a strategy the synthetic sector has already implemented successfully.

This article is part of the Rapaport Diamond Price Statistics Annual Report. To see the full data breakdown for 2025, click here.

Main image: Shutterstock