With an air of confidence, executives of Signet Jewelers stepped up to the podium during the company’s investor day at the New York Stock Exchange (NYSE) in April. The company has experienced an impressive few years since the pandemic, accumulating steady gains in its stock price and revenue, both of which are considered bellwethers for the broader industry.

Signet’s growth came via acquisitions — mainly bolstering its e-commerce capabilities — and organically, driven by its use of data analytics to identify growth opportunities.

With each of its banners strategically positioned to target specific consumer segments and trends, the company is bullish moving forward. It is determined to capitalize on the changes currently underway in the jewelry sector.

“The jewelry category is highly fragmented because it has been historically driven by physical brick-and-mortar presence and local relationships,” CEO Gina Drosos emphasized in her opening remarks to investors. “As the only scaled player, we’re investing to disrupt this historical construct with scaled capabilities including digital and data and a unified retail experience that would be very hard, if not impossible, for others to match.”

Drosos inadvertently threw down the gauntlet for the rest of the jewelry retail space. While independents represent approximately two-thirds of specialty jewelry sales, according to Signet’s estimates, she foresees that segment contracting. Signet is aiming to take advantage of that and raise its share to 12% of the US jewelry market within five years from its current 9.7%. In 2019, it held around 6%.

The group outlined four areas that would drive growth in the medium term:

- A strong rebound in the bridal segment,

which is still reeling from the Covid-19 disruption. - Rising demand for accessible luxury — high-quality, affordable jewelry for milestone occasions.

- An opportunity for its services business to enhance the jewelry ownership experience, through its loyalty programs as well as repair, customization, and financing offerings.

- Stimulating gains from its marketing, digital and data capabilities.

Independent core

None of this was news to the rest of the trade, particularly the top-tier family-owned independent jewelers that have also seen robust sales growth since Covid-19. Those focus areas have formed the core of their business for decades, although they were lagging in their use of data analytics. While they don’t have the budget and scale that Signet enjoys, they’re confident in their own competitive edge.

“Their advantage is their ability to create a personalized experience for the consumer and push their own store brand,” says Dave Bonaparte, president of Jewelers of America (JA), which advocates on behalf of the jewelry trade. “Their store brand is the most important thing they have going for them, because that’s how they build trust.”

Bonaparte acknowledges some vulnerabilities among independents. With the composition of that sector set to recalibrate, as Drosos predicted, succession planning — or the lack thereof — is the single biggest challenge independents face, according to Bonaparte. That is, as baby boomer jewelers prepare to retire, many don’t have a family member willing to take over.

The jewelry category is highly fragmented because it has been historically driven by physical brick-and-mortar presence and local relationships…. We’re investing to disrupt this historical construct.

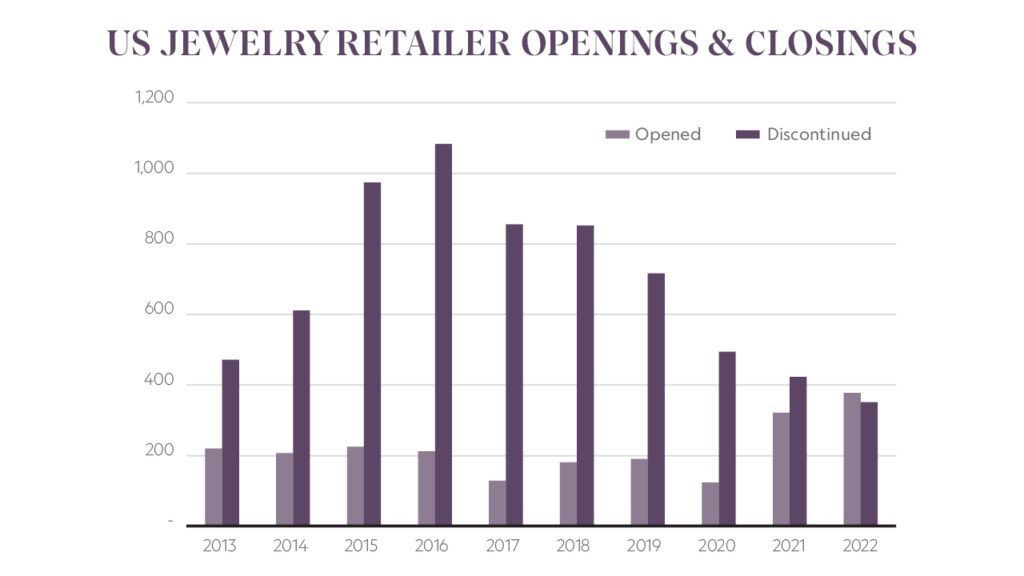

It’s also not an easy business to sell, he explains, considering you’re packaging receivables, inventory, and the brand. As a result, many simply close their doors when the time comes to move on, as noted in the quarterly data from the Jewelers Board of Trade (JBT), which provides credit scores for jewelry businesses.

The vast majority of jewelry companies that were discontinued in the past several years have been those that simply shut, according to the JBT. Of the 353 discontinued jewelry retail businesses it recorded last year, 272 ceased operations, while 80 were the result of a sale or merger and one filed for bankruptcy, the organization’s data showed.

Meanwhile, 379 new jewelry retail businesses were registered in 2022, marking the first time in many years that openings exceeded closures, Bonaparte notes. “That’s an optimistic sign that independents are coming back,” he says. “There’s still a large population of independent jewelers out there, which is not going to change anytime soon.”

Personalized digital

The new businesses aren’t just e-commerce, as many might think, Bonaparte continues. While there are a lot of online retailers selling jewelry, businesses still want a physical location.

Although the pandemic pushed consumers online, giving digital sales a massive boost, there has since been a strong return to in-store purchases. In fact, shoppers prefer brick-and-mortar, particularly for items above $500, according to Jordan Peck, director of operations at New York-based jewelry brand Brevani and cochair of The Plumb Club’s market-research committee.

A survey by The Plumb Club — a coalition of suppliers to the jewelry, diamond and watch industries — revealed a major increase in the desire for a seamless and convenient experience from online to in-store, Peck reported in a recent webinar the organization hosted. The full research is scheduled to be published during the JCK Las Vegas show at the beginning of June.

Diversity, inclusivity, responsible business practice, the use of technology, [and] emotional selling are all tools the jeweler must use to tap the consumer mind-set.

Digital innovation is not solely online; it is in our stores. Digital and in-store customers are the same people. They require fluid and consistent movement across all our channels.

Independents are starting to incorporate technology into all aspects of omni-channel, but they are still a step behind in terms of their capabilities, Bonaparte admits. It’s an area in which Signet is investing heavily to engage with customers on all possible platforms.

Omni-channel has therefore taken on a new meaning, involving greater integration between the digital and physical platforms.

“Digital innovation is not solely online; it is in our stores,” said Rebecca Wooters, Signet’s chief digital officer, at the NYSE investor day. “Digital and in-store customers are the same people. They require fluid and consistent movement across all our channels.”

The company is focused on personalizing the digital experience, Wooters continued. It is investing in artificial intelligence to enhance its online engagement, and it is immersed in data analytics to track its customers’ interests and tastes across all channels. That way, she pointed out, Signet can curate its service for customers wherever they might appear.

“We believe the scale and sophistication of our data, tech and analytics are beyond what any independent can build and is increasingly a driver of share growth,” emphasized Jamie Singleton, Signet’s group president and chief operating officer.

Independents might not have the same capacity to do that, Bonaparte acknowledges, but they are using technology to market and sell. And while it’s difficult for jewelers to replicate the brick-and-mortar experience online, there is a growing awareness of the need “to be as close as possible to the person on the other side of the screen,” Peck observed.

Panelists in The Plumb Club webinar noted the importance of having a clear website; an authentic social-media presence, particularly on Facebook and Instagram; and a cohesiveness among all of one’s platforms. It’s not just about the online presence, argued Steven Lerche, chief operating officer of jewelry wholesaler Goldstar and cochair of The Plumb Club’s market research committee. “It’s about how easy it is for the consumer to find the jeweler and how effectively the jeweler can keep them engaged.”

Generational shift

Online engagement ranked among the key purchase drivers in The Plumb Club’s survey, Lerche noted, with Peck reporting that an estimated 13% of jewelry sales took place online.

But more importantly, online has a massive impact in getting the customer to the store, as younger consumers are using their digital prowess to research their purchases before going to the brick-and-mortar location.

That said, the in-store experience is even more vital to consumers, The Plumb Club’s research suggested. In the study, 79% of consumers said the look of a retail shop affected their jewelry purchases. A salesperson’s credentials also factored high in the criteria driving the sale. The retailer’s commitment to sustainability drew in 71% of consumers, while 69% of respondents said they would be willing to pay more for a retailer’s demonstration of diversity and inclusion.

“Consumers want to see themselves reflected in the brand,” said Plumb Club executive director Lawrence Hess in the webinar. “Diversity, inclusivity, responsible business practice, the use of technology, [and] emotional selling are all tools the jeweler must use to tap the consumer mind-set.”

Purchases influenced by environmentally and socially responsible business practices are expected to triple in the next few years, Lerche added.

Inclusive retail

The prominence of those issues marks a significant change in buying habits. As the baby boomer generation leaves the arena, the generations that follow them — Gen X, millennials and Gen Z — have a changed view of the world, and a very different outlook on jewelry and how to acquire it, Hess explained.

The customer base is also constantly evolving, with a sharp rise in female self-purchases and increasing demand in the LGBTQ community, while Hispanic and Black, Indigenous, and people of color (BIPOC) consumers also represent a significant growth opportunity. That diverse customer base needs to be represented in the store as well, The Plumb Club stressed.

“These are no longer buzz words,” explained Michael O’Connor, the club’s marketing director. “Consumers feel a retailer’s commitment to sustainability, and it is important that the retailer actually demonstrates diversity and inclusivity. These are purchasing triggers that should drive jewelers to embrace them.”

For its part, Signet has recognized the need to demonstrate diversity and inclusivity. It has radically changed the makeup of its board in the past five years, with many senior positions occupied by women — who accounted for five of the six presenters at the investor day.

The emphasis on inclusivity further shows a recognition that jewelers can no longer take their customers for granted. At the very least, the presentation by Signet and the research by The Plumb Club reveal that jewelers want to better understand the ever-evolving consumer — what customers want, where they are, and how they intend to make the final purchase.

Signet refers to its access to consumers as its secret weapon. The company’s use of tech is bringing it closer to the person on the street, while independents are using their personalized in-store service to maintain their position, Bonaparte suggests.

The majors and the independents are targeting each other’s competitive advantages in the battle for growth and market share. That may be a net positive for the broader jewelry market.

This article is from the May-June 2023 issue of Rapaport Magazine. View other articles here.

Image: Focus on US jewelers (Shutterstock).